I was at the Media Guardian Radio Reborn conference last week, and Claire Enders showed us one of those scary “share of display advertising” graphs. True to form, every sector was either in decline or clearly looking a bit feeble (radio in the latter group). The share of spend was on the vertical axis, and the sectors (TV, National Press, Regional Press, Radio…) along the horizontal access, although “Outdoor” was inexplicably absent.

The only set of bars in growth was the set labelled “Internet”.

But this strikes me as being wrong; it’s an invalid comparison. “The Internet” is just a set of interconnecting networks, using an agreed communication protocol. There’s no business called “The Internet Ltd/plc” (although doubtless Google are working on that right now).

A more accurate set of labels would have been: “ITV & other commercial TV operators”, “Guardian & other national newspaper publishers”, “GCap Media plc & other commercial radio operators”, and… “Google & other search engines”. That would be a far more accurate indication of where the money is going. Money doesn’t go “to the Internet” – it goes to companies who have used “The Internet” as a platform to access consumers that they were previously unable to.

What a more accurately labelled graph would show us is that advertisers are moving their money to where they feel it is more effective, a feeling that’s re-enforced by apparently magical accountability for every display and click. (Can you tell that I’m sceptical?). The problem isn’t “The Internet”; the problem is that traditional media owners have failed to keep up with their clients’ demands, or (and probably more realistically), educated their clients to have more reasonable demands.

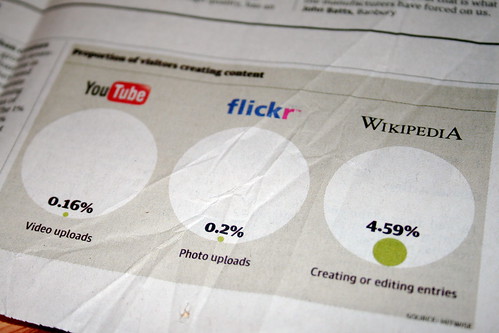

Google & Co. have a substantial audience. OFCOM tells us that 65% of the UK have “The Internet” (of which 86% apparently have “Broadband”, whatever that means). Here’s what’s interesting – whilst the content consumption on the Internet is fragmented beyond belief (and this blog contributes yet another consumption pin-prick on the map), the commercialisation and aggregration of that audience is in the hands of a much smaller number of media sellers. So actually, what Claire was really trying to tell us is that advertisers trust Google to deliver better results on a “per click” model or multimedia display model, than they do with incumbent TV, Radio or Newspaper companies.

The challenge for incumbent media owners is to change the perception of advertisers about “The Internet”. Some of that needs to be through real, demonstrable, product development, and clawing back some of people’s media consumption time that is now spent with Google, Facebook, et al. Incumbents allowed competitors to steal audience from right under their noses because they didn’t think “The Internet” would ever be a platform of significant reach. Now it’s up at 65% coverage, compared with ~90% for TV and Radio, and 50%-60% for Newspapers (national readership survey).

But the second challenge is to offer a commercial proposition that is attractive to those starry-eyed about “Internet” advertising. That’s a mix of really good, effective, communication with consumers, and believable and trustworthy measurement.

I think it’s amazing how much trouble Kelvin Mackenzie caused the radio industry by selfishly trying to derail RAJAR by claiming it was inaccurate. One person created an environment of anxiety about the reliability of RAJAR’s measurements, but everyone apparently finds Google utterly trustworthy and really truly believes that they measure every click and every ad delivery. Maybe they should look at some of the Javascript that delivers the ads, or work how many splogs there are out there? Or survey how many people have ad-blockers? I’m not trying to undermine the on-line advertising ecosystem, but there needs to be some reality about the fallibility of any system.

The radio platform is used by 90% of the population, and commercial radio used by 62% of adults. Commercial radio is about at parity with “The Internet” in terms of reach, but ahead on time spent consuming. With Digital Radio we have a platform that’s capable of delivering a similar digital advertising environment as “The Internet” platform, but is still far more ubiquitous in every part of life. I believe we’re still a long way off, in behaviour terms, people using “The Internet” in the kitchen, bathroom, bedroom; and thankfully economics will continue to make using “The Internet” in mobile environments a great deal more expensive than receiving digital radio. So if we can use Digital Radio to deliver advertising propositions that are the same as the ones delivered on “The Internet”, that can be measured as reliably, and are demonstrably as effective, we stand a chance of revitalising interest in what radio companies can offer advertisers.